With a growing middle class, rising Internet penetration, and a population of nearly 100 million people, most of whom are young and tech-savvy, Vietnam has all the needed characteristics to become a major fintech market.

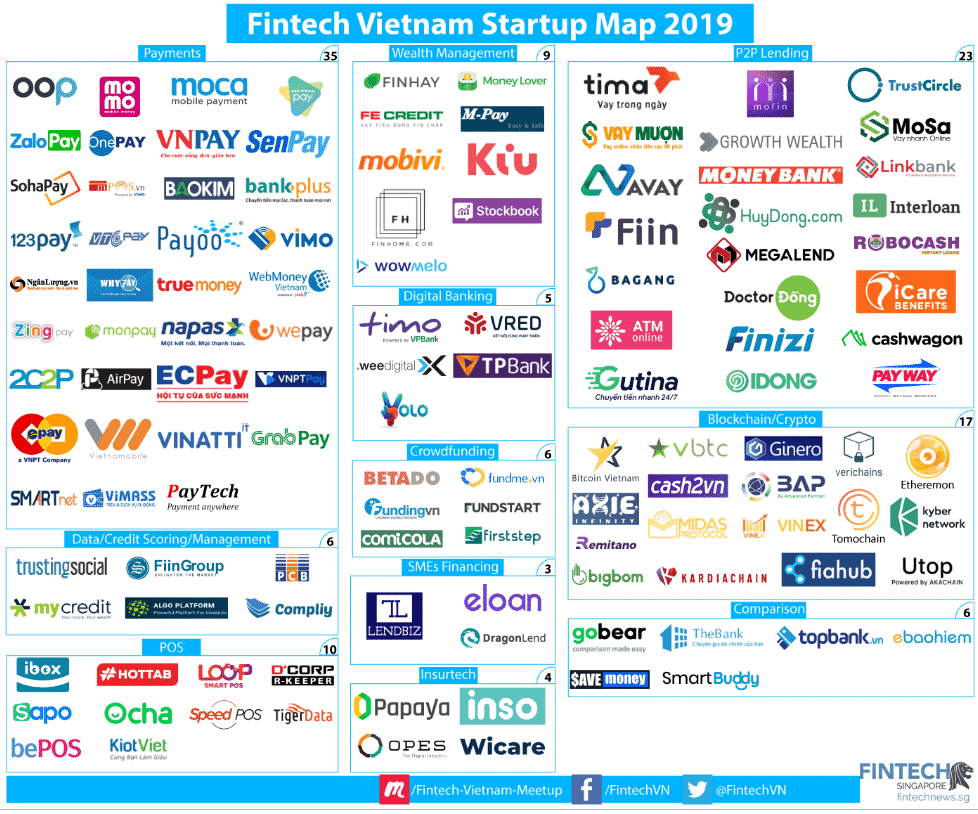

In the past years, the Vietnamese fintech startup ecosystem has witnessed significant growth and is now home to some 120 companies and brands covering a broad range of services, from digital payments and alternative finance, to wealth management and blockchain.

With 35 startups and platforms, payments is the most populous fintech segment. Notable companies and brands in this segment include M_Service, the developer of mobile payments app MoMo and one of the most well-funded fintech startups in Vietnam, Moca, a free mobile payment application for Vietnamese consumers, GrabPay, a mobile wallet integrated into Grab’s app in Vietnam, and ZION, the company behind Zalo Pay, a service integrated with Vietnam’s popular messaging platform Zalo that lets users link a payment card to make P2P payments, pay via NFC, QR codes, as well as purchase products and services online, mobile topups, and pay their utility bills.

Peer-to-peer (P2P) lending is the second largest fintech segment in Vietnam with over 20 startups. Players and solutions in the area include Tima, a consumer financial marketplace and P2P lending platform, Growth Wealth, a P2P lending platform for small and medium-sized enterprises (SMEs) in Vietnam, as well as TrustCircle, and Vay Muon.

Blockchain and cryptocurrency is another area that’s witnessed significant traction in the past years. Since the launch of Bitcoin Vietnam, the country’s first bitcoin broker exchange, in 2014, several companies have emerged to tap into the blockchain and crypto frenzy. These include TomoChain, a public blockchain promising faster and cheaper transactions designed to support decentralized applications, and Kyber Network, an on-chain liquidity protocol that aggregates liquidity from a wide range of reserves, enabling instant and secure token exchange in decentralized applications.

Other segments present in the Vietnamese market include comparison platforms, with players such as TheBank and ebaohiem, insurtech, with players like Papaya, Inso and Wicare, as well as point-of-sale (POS) system providers like bePOS, wealth management platform like Finsify, digital banking platforms like Timo, and credit scoring startups like TrustingSocial.

Facilitating fintech development

Vietnam’s rapidly growing payments industry coincides with the boom of cashless payments, which more than doubled in value over the first three quarters of 2018. In particular, transactions over mobile apps and digital wallets rose by an impressive 126% and 161%, respectively, according to Department of Payments at the State Bank of Vietnam.

A report published in late 2018 by Allied Market Research estimates that the Vietnamese mobile payments market could reach US$70,937 million by 2025, growing at a CAGR of 18.2% from 2018 to 2025.

Major factors set to contribute to the growth of the market include changes in customer preference from cash to digital payments, surge in need for immediate transactions in Vietnam, increased penetration of internet and smartphones, and growth of the e-commerce industry.

It also correlates with the government’s ambition to develop non-cash payments.

In January 2017, a policy decision was signed with the goal to reduce the ratio of cash transactions to 10% and have at least 70% of the population with a bank account by 2020. It was followed a few months after by the establishment of the Fintech Steering Committee by the State Bank of Vietnam to advise the government on ecosystem development.

Moving forward, industry observers and experts are advising for the creation of a regulatory sandbox that would allow financial firms and fintech companies to test out innovative products.

According to Nguyen Thanh Binh, acting discipline lead at the economics and finance department of RMIT University, the existing legal framework in Vietnam is unclear and does not cover the development and penetration of new technological products. A regulatory sandbox would help Vietnamese fintech companies and startups hasten their development, he said last month during a seminar.

Nguyen The Hien, sales director at the Ho Chi Minh City-based telecommunications firm VHT, agrees, adding that a regulatory sandbox would also allow the government to keep up with emerging technologies and improve its supervision over the industry.

“As technology changes rapidly, the sandbox will help local tech firms operate more easily and the Government improve its control over new technologies,” Hien told Vietnam News.

“Any tech firms that are incapable of producing and testing their own technologies will be removed from the sandbox, so it would improve the Government’s supervision over the Vietnamese technology industry.”

Source: fintechnews.sg

Contact experts at Innotech Vietnamfor any questions about Software outsourcing for Fintech!

Email: [email protected]