Going digital is no longer the hard part of banking and insurance. Your customers crossed that line years ago. The hard part now is becoming AI-native — capturing the value of artificial intelligence without breaking the three things a financial institution can never break: risk, compliance, and trust.

For a decade, the BFSI conversation was about channels: mobile apps, internet banking, digital onboarding, e-wallets. That race is largely settled. The next race — the new BFSI era — is about intelligence: how institutions turn their data into decisions across every product and every operation, safely and at scale.

This is where most institutions are stuck. The ambition is there. The budget is there. What’s missing is a way to move from scattered AI experiments to an AI capability the whole organisation can rely on. This article lays out what’s changing, why it matters to your P&L and your regulator, and how a BFSI-native transformation partner helps you cross the gap.

BFSI is moving through three eras — and the leaders in the region have already started the third.

The next BFSI era is no longer only about digital channels, but about secure AI-native capability across banking, insurance and fintech operations.

1. BFSI Is Entering Its Third Era: Traditional → Digital → AI-Native

Every bank and insurer is somewhere on a three-stage journey.

- Traditional BFSI — branch-led, product-centric, manual operations, optimised for stability.

- Digital BFSI — channel-led, customer-centric, automated processes, optimised for convenience and cost. Most institutions in the region are here.

- AI-Native BFSI — intelligence-led, decision-centric, autonomous and augmented operations, optimised for adaptive speed and personalisation at scale.

The third era is not a forecast. It is already visible: in Korea, the digital-only KakaoBank — with around 25 million customers, about half the country’s population — has publicly repositioned itself as an “AI-native bank.” When the regional challenger redefines itself around AI, “wait and see” quietly becomes a competitive risk.

The strategic question is no longer “should we adopt AI?”[Text Wrapping Break]It is “will we become AI-native deliberately and safely — or reactively, after a competitor does it first?”

2. The Demand Is Already Here — Readiness Is the Constraint

The numbers across Innotech’s priority markets tell one story: customers have gone digital faster than most institutions can re-platform.

- Vietnam recorded around 17.7 billion cashless transactions in 2024, up 56% year on year, with 87% of adults now holding bank accounts and QR payments the fastest-growing rail (State Bank of Vietnam, 2024–2025).

- In the Philippines, digital payments reached 57.4% of retail transaction volume in 2024, already ahead of plan, with a national target of 60–70% by 2028 (Bangko Sentral ng Pilipinas, 2025).

- Singapore remains the regional benchmark for digital-bank licensing and cross-border real-time rails.

So the bottleneck has shifted. It is no longer “will customers use digital?” — they already do. It is “can the institution keep pace with its own customers?” That is a capability problem, and capability is something you can build with the right partner.

3. Why the Old Operating Model Can’t Capture the New Value

The prize is enormous. Generative AI alone could add US$200–340 billion in value to global banking every year — equivalent to 9–15% of operating profit — and a further US$50–70 billion to insurance (McKinsey Global Institute, 2023). Financial services is now forecast to be the single largest AI-spending industry, more than 20% of all AI spending, as the global market more than doubles toward US$632 billion by 2028 (IDC, 2024).

Yet most institutions can’t capture it, because six structural constraints get in the way: legacy core systems, fragmented customer experience, rising compliance load, high operating costs, data silos, and slow time-to-market. Of these, data silos are the hinge — trapped, disconnected data is both the cause of today’s inefficiency and the reason most AI projects quietly die.

The evidence is sobering. While 65% of organisations now regularly use generative AI, only about a third have scaled it, and fewer than 20% track its KPIs (McKinsey, 2024–2025). Independent research found that 95% of generative-AI pilots never reach meaningful profit-and-loss impact (MIT Project NANDA, 2025). In banking specifically, only 8% of institutions run generative AI strategically while 78% remain at the tactical, experimental stage (IBM Institute for Business Value, 2025).

The lesson is clear: AI value does not come from buying a model. It comes from changing the operating model.

4. AI Is Becoming an Enterprise Layer, Not a Feature

Here is the single most important architectural idea of the new BFSI era.

If you treat AI as a feature — a chatbot here, a pilot there — you end up with a graveyard of disconnected experiments. That’s the two-thirds that never scale. If instead you treat AI as a layer — a governed, shared intelligence capability that runs across every channel, sector solution, and operation, and turns your data into decisions wherever they’re needed — the value compounds.

Just as cloud became a layer and data became a layer, AI is now becoming the decision and intelligence layer of the institution. That architectural choice — layer, not feature — is worth more than any single AI model you could buy. And it only works on a clean, connected data platform: no governed data, no enterprise AI.

AI creates value in BFSI when it becomes a governed enterprise layer connected to data, channels, workflows and compliance controls.

5. The Four Pillars of AI Transformation for BFSI

Sustainable AI value rests on four pillars moving together — what we call AX (AI Transformation):

| Pillar | What it means in BFSI |

| People | Roles, skills, change management, human-in-the-loop design. Adoption — not the model — is the real bottleneck. |

| Process | Redesign workflows around AI. Winners rebuild processes; they don’t bolt AI onto old ones. |

| Technology | The AI layer, the data platform, and the integration beneath it. |

| Governance | Model risk, explainability, data privacy and residency, regulatory alignment. |

In banking and insurance, Governance is non-negotiable. Skipping it is not an inefficiency — it is a regulatory incident. This is exactly why so many programmes stall: McKinsey found that roughly 47% of organisations have already experienced at least one negative consequence from generative AI (2025). Done right, all four pillars turn AI from a risk into a durable advantage.

6. High-Value AI Use Cases Across Banking, Insurance, Consumer Finance, and Fintech

The institutions that win don’t try to boil the ocean. They sequence by business value and feasibility, starting where value is high and the path is clear. Below are the use cases that consistently move the P&L, by segment.

Banking

| AI use case | Business value |

| Customer-service assistants | Resolve routine queries at scale; lower cost-to-serve, higher satisfaction |

| Fraud & AML analytics | Detect anomalies in real time; reduce losses and false positives |

| Credit decisioning & document processing | Faster, more consistent lending decisions with a clear audit trail |

| Engineering & operations copilots | Higher developer and back-office productivity |

Insurance

| AI use case | Business value |

| Claims document intelligence | Straight-through claims; lower leakage and faster settlement |

| Underwriting support & risk scoring | Better risk selection and pricing accuracy |

| Agent & adviser copilots | Higher producer productivity and consistency |

Consumer Finance

| AI use case | Business value |

| Automated origination & onboarding | Growth at the point of sale, with controlled risk |

| Collections optimisation | Protected portfolio quality at lower cost |

| High-volume customer service | Satisfaction at scale across millions of small accounts |

Fintech

| AI use case | Business value |

| KYC & identity automation | Faster onboarding that still satisfies the regulator |

| Transaction-fraud detection | Real-time protection of the rails |

| Embedded support & personalisation | Higher engagement and conversion |

These are not speculative. In financial services, document-processing agents reached around 53% adoption in the first year they were measured (NVIDIA, 2024–2025). And the risk side is just as urgent: deepfake-enabled fraud attempts rose by more than 2,137% over three years (Signicat, 2025), making AI-powered fraud analytics a defensive necessity, not a nice-to-have.

7. Innotech’s BFSI AI Capability: From LLM Customization to Agentic AI

Positioning around the new BFSI era only means something if it rests on concrete capability, not generic AI claims. Innotech connects its AI positioning to services built for regulated institutions.

7.1 LLM Customization for Banking and Insurance

Most institutions don’t need a generic large language model. They need AI that understands their data, products, terminology, policies, and compliance rules. A customized LLM solution can power internal knowledge search, customer-support automation, document processing, compliance checking, and enterprise reporting — grounded in the institution’s own data and kept inside its own boundary. The challenge isn’t model performance; it’s making the model useful, secure, and aligned with how the business actually runs.

7.2 Agentic AI for Regulated Workflows

Unlike a simple chatbot, agentic AI can plan actions, call tools, coordinate multi-step workflows, retain context, and interact with core systems — under human-in-the-loop approval and guardrails. In BFSI that maps directly to high-value, multi-step operations: claims handling, customer onboarding, collections, and reconciliation. Crucially, this is not “an AI feature” — it is an engineering system that needs orchestration, memory, security, integration, and monitoring. That is precisely where engineering discipline separates a production system from a demo.

7.3 Document Intelligence, Fraud, and Risk Analytics

Three capabilities repay investment fastest in banking and insurance: document intelligence (extracting and classifying data from forms, policies, statements, and contracts), fraud analytics (catching anomalies and synthetic identities in real time), and risk analytics (sharper credit and underwriting decisions). Innotech delivers these through its Generative AI and AI development practices — including domain-specific applications such as AI for health-insurance claims management.

The point is consistent: AI is only valuable when it is connected to real business systems. That is the difference between an AI demo and an AI-native institution.

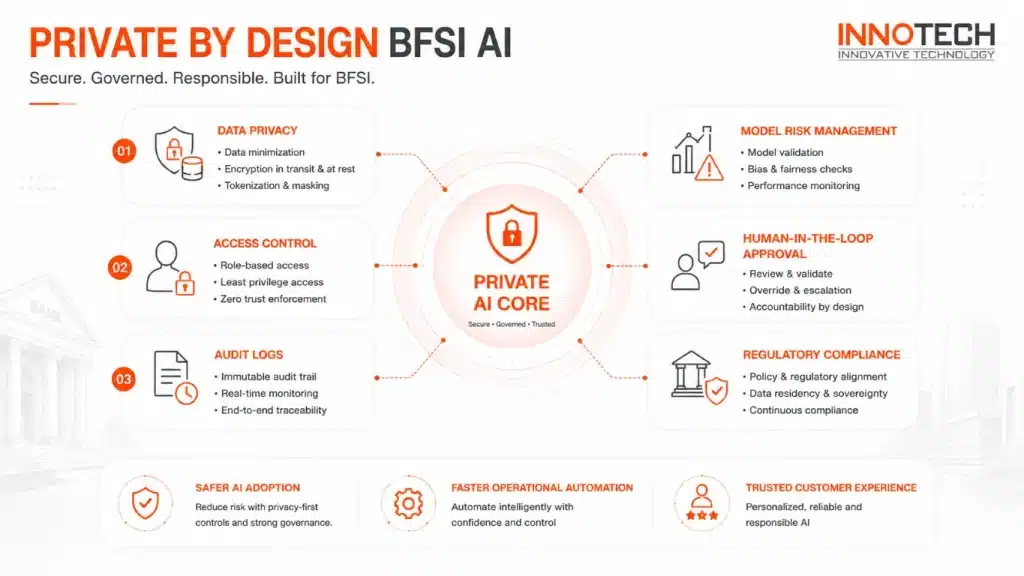

8. Why “Private by Design” Is Now the Law, Not a Preference

In BFSI, AI cannot run wherever it’s most convenient. It must run inside the institution’s control boundary — private, governed, and auditable by design.

This is no longer just good practice; in Vietnam it is becoming law. The Law on Artificial Intelligence (No. 134/2025/QH15) takes effect on 1 March 2026 and classifies AI systems into three risk tiers, while the Cybersecurity Law (No. 116/2025/QH15) takes effect on 1 July 2026. Together they make control over data and decisions a legal requirement, not a design option. The market is already moving in this direction: 95% of organisations say private or sovereign AI is important (NTT Data, 2026), and a majority of BFSI firms now plan to build their own large language model capability (TCS).

A modern enterprise AI architecture for BFSI therefore wraps governance and security around every layer — access control, audit logging, model-risk management, explainability, and PII protection — from the data sources, through a private data platform and model layer, up to the assistants and agents your people actually use. That is how an institution gets capability and control, instead of trading one for the other.

9. A Staged, De-risked Path: Discover → Pilot → Scale → Transform

The fastest way to fail is to bet the institution on one big AI programme. The right approach is a gated journey, where each stage proves value before the next is funded.

| Stage | Focus | Success metrics (the buyer’s KPIs) |

| Discover | Readiness assessment, data review, use-case prioritisation | Prioritised use cases · data-readiness score · target ROI |

| Pilot | Build 1–3 high-value use cases on a private AI architecture | Quality vs. baseline · cycle-time reduction · user adoption |

| Scale | Productionise, integrate, govern, change-manage | Cost-to-serve ↓ · straight-through rate ↑ · EBIT contribution |

| Transform | AI as an enterprise layer + a continuous use-case factory | Revenue impact · % of processes AI-enabled · risk incidents ↓ |

Notice that the metrics are business metrics — cost-to-income, cycle time, fraud loss, customer satisfaction — not model accuracy. That directly addresses the reason most programmes lose the boardroom: fewer than 20% of organisations track the KPIs that matter (McKinsey, 2025).

10. How the New BFSI Era Plays Out Across the Region

The new BFSI era doesn’t look identical in every market. Each has a different starting point, regulatory posture, and competitive pressure — and the AI agenda should be framed accordingly.

Vietnam — compliant, private AI on a modern core. With cashless payments surging and a domestic AI market projected to grow from roughly US$554 million in 2023 toward US$1.5 billion by 2030, demand is strong — but the new AI and cybersecurity laws raise the bar on data control. The strongest positioning here is private, compliant AI built on a modernised core and digital-wallet infrastructure, where governance is designed in from day one.

Philippines — automation for financial inclusion at scale. Consumer finance and digital payments are expanding fast, and the market is defined by high-volume, low-ticket lending to millions of customers. The strongest positioning is AI-driven origination, KYC, collections, and customer service that lower cost-to-serve while protecting portfolio quality — turning scale into margin.

Singapore — enterprise-grade, governed AI. As the region’s most sophisticated regulatory and digital-banking hub, Singapore rewards rigour. The strongest positioning is governed, auditable enterprise AI for real-time payments, risk, and cross-border services, where explainability and model-risk management are first-class requirements.

Korea — AI-native customer experience. With AI-native challengers already at scale, the competitive frontier is hyper-personalisation. The strongest positioning is agentic AI and adaptive personalisation that match challenger-bank experiences without compromising trust.

Across all four, the common thread is the same: capture AI value without breaking risk, compliance, or customer trust.

11. What Makes Innotech Different from a Generic AI Vendor

Many vendors now claim they can “do AI.” Few have the foundation that BFSI actually demands. What sets Innotech apart is not one capability — it is the combination.

| Differentiator | Why it matters in BFSI |

| Enterprise & core-system delivery | Handles production systems carrying real money and risk, not just prototypes |

| Banking, insurance & consumer-finance domain depth | We speak risk, compliance, and the value chain — not only code |

| Governance-first, private AI | Aligns with data-residency law and model-risk expectations |

| Full lifecycle delivery | Architecture, build, QA, DevSecOps, and run — one accountable partner |

| LLM + Agentic AI capability | Matches the new enterprise AI demand, not last year’s chatbot |

| In-region presence (VN/PH/SG/KR) | Understands local rails, regulators, and customer behaviour |

| Outcome-based engagement | Value- and SLA-aligned, not billable-hours staff augmentation |

A generic vendor can build a prototype. An AI-native institution needs a partner that can take it from prototype to production — securely, compliantly, and at scale.

12. Why Innotech: Digital Transformation + AI Transformation

Plenty of firms can show you a chatbot. Very few have also put a bank’s core in the cloud. The combination is the point.

Innotech Vietnam is a BFSI-native transformation partner with 200+ projects delivered, a 90%+ client return rate, and 200+ engineers and domain experts across four delivery centres. More importantly, we’ve earned trust where it’s hardest to earn — building and running mission-critical systems for banks, insurers, and fintechs, including TymeBank, ACB, Manulife, Groupama, Commonwealth Bank, and Unifimoney.

The market is moving:

from a software outsourcing vendor[Text Wrapping Break]to an AI & digital transformation partner that helps financial institutions become AI-native — safely.

That is the combination AI without delivery discipline can’t offer (it’s just a demo) and delivery without AI can’t offer (it’s yesterday’s partner).

13. Behind It: Innotech’s AI Innovation Hub

Behind this positioning is a dedicated AI Innovation Hub — a young, adaptive, high-calibre team of engineers, AI developers, solution architects, and business analysts whose focus is not experiments for their own sake, but production-ready solutions that improve operational efficiency, automate repetitive work, and create measurable business value. In a market where models, frameworks, and use cases evolve monthly, that adaptability — paired with delivery discipline — is exactly what lets a financial institution move from AI exploration to real implementation with confidence.

14. Frequently Asked Questions About the New BFSI Era

What does “AI-native BFSI” actually mean?

An AI-native bank or insurer doesn’t bolt AI onto existing processes — it runs on intelligence. Decisions, operations, and customer journeys are designed around a governed AI layer that turns the institution’s own data into action. It is the third stage after traditional (branch-led) and digital (channel-led) banking.

Is AI transformation different from digital transformation?

Yes. Digital transformation moved the institution onto modern channels and automated workflows. AI transformation goes a layer deeper: it makes those workflows decide and adapt. The two are sequential — the clean data and cloud foundation built during digital transformation is exactly what AI transformation needs to work.

Why do so many BFSI AI projects fail to scale?

Because they are treated as isolated features, not as a shared, governed capability. The evidence is stark: about 65% of organisations use generative AI, but only a third have scaled it, and roughly 95% of pilots never reach meaningful P&L impact (McKinsey; MIT Project NANDA, 2025). The fix is architectural — an enterprise AI layer on a real data platform — plus governance and business-level KPIs.

What is “private AI,” and why does it matter for banks and insurers?

Private (or sovereign) AI keeps data, models, and decisions inside the institution’s control boundary, with full auditability — instead of sending sensitive information to a public service. For BFSI it is now close to mandatory: 95% of organisations call private or sovereign AI important (NTT Data, 2026), and in Vietnam the AI Law (effective 1 March 2026) and Cybersecurity Law (effective 1 July 2026) make control over data and decisions a legal requirement.

Where should a bank or insurer start?

Not with a moonshot. Start with a readiness and opportunity assessment, prioritise two or three use cases that are both high-value and high-feasibility, and prove them in a contained pilot before scaling. Each stage should pass a go/no-go gate measured in business KPIs — cost-to-income, cycle time, fraud loss, and customer satisfaction.

How is Innotech different from a generic AI outsourcing vendor?

The difference is the combination: proven banking, insurance, and fintech delivery; a governance-first, private-AI approach aligned with new data-residency law; full-lifecycle delivery from architecture to run; and in-region presence across Vietnam, the Philippines, Singapore, and Korea. A generic vendor can build a prototype; an AI-native institution needs a partner that can take it to production safely.

15. Build the New BFSI Era with Innotech

The next decade of banking and insurance won’t be won by whoever ships the most pilots. It will be won by institutions that treat AI as a governed enterprise layer, redesign their processes around it, keep it private and compliant by design, and measure it against the metrics the board actually cares about.

If your institution is ready to move from digital to AI-native — without compromising risk, compliance, or customer trust — Innotech Vietnam can help you build the foundation, the AI layer, and the roadmap to get there.

For BFSI institutions, AI needs to be private, governed and auditable by design, especially when it touches customer data, risk decisions and regulated workflows.

Talk to Innotech Vietnam about a focused AI & Digital Transformation Assessment for your bank, insurer, or consumer-finance business — and start the new BFSI era with a clear, de-risked first step.

Contact Innotech Vietnam →